What are Tokenomics

So much about the crypto ecosystem is novel and disruptive, including its vocabulary, which features entirely new words, invented to describe entirely new concepts. Tokenomics is a great example. It is what is known as a portmanteau, a word that blends the meaning of two other words – tokens and economics. It fills the empty space in the dictionary to describe how the mechanics of cryptocurrency function – supply, distribution and incentive structure – relate to value.

The choice of the term tokenomics’ constituent parts – token and economics – may seem a bit confusing if your assumption is that cryptocurrencies are simply new forms of internet money. In reality, crypto can apply to any form of value transfer.

This is why the word token is used, because units of cryptocurrency value can function as money, but also give the holder specific utility. Just as a games arcade or laundromat may require that you use a specific token to operate their machines, many blockchain based services will be powered by their own token, which unlocks specific privileges or rewards:

- DEFI – users are rewarded with tokens for activity (borrowing/lending), or tokens are created as synthetic versions of other existing cryptocurrencies

- DAOs – token holders get voting rights within Decentralised Autonomous Organisations, new digital communities governed by Smart Contracts

- Gaming/Metaverse – where game activity and in-game items are represented by tokens and can have exchangeable value

If we add this understanding of cryptocurrency as tokens, to the traditional definition of economics – measuring the production, distribution and consumption of goods and services – we can breakdown what tokenomics within cryptocurrency measures into:

- how tokens are produced via their supply schedule, using a specific set of supply metrics

- how tokens are distributed among holders

- the incentives that encourage usage and ownership of tokens

We can start to unpack these aspects of tokenomics by looking at the supply schedule for the first ever cryptocurrency, Bitcoin.

1. Supply schedule

Bitcoin went live in January 2009, based on a set of rules – the Bitcoin Protocol – that included a clearly defined supply schedule:

- New bitcoins are created through Mining. Miners compete to process a new block of transactions by committing computing power to solve a mathematical puzzle. They do this by running a set algorithm hoping to find the answer – this is known as Proof of Work.

- A new block is mined roughly every ten minutes. The system is self-regulating, through a difficulty adjustment of the mining algorithm every two weeks, to maintain the steady rate of block creation.

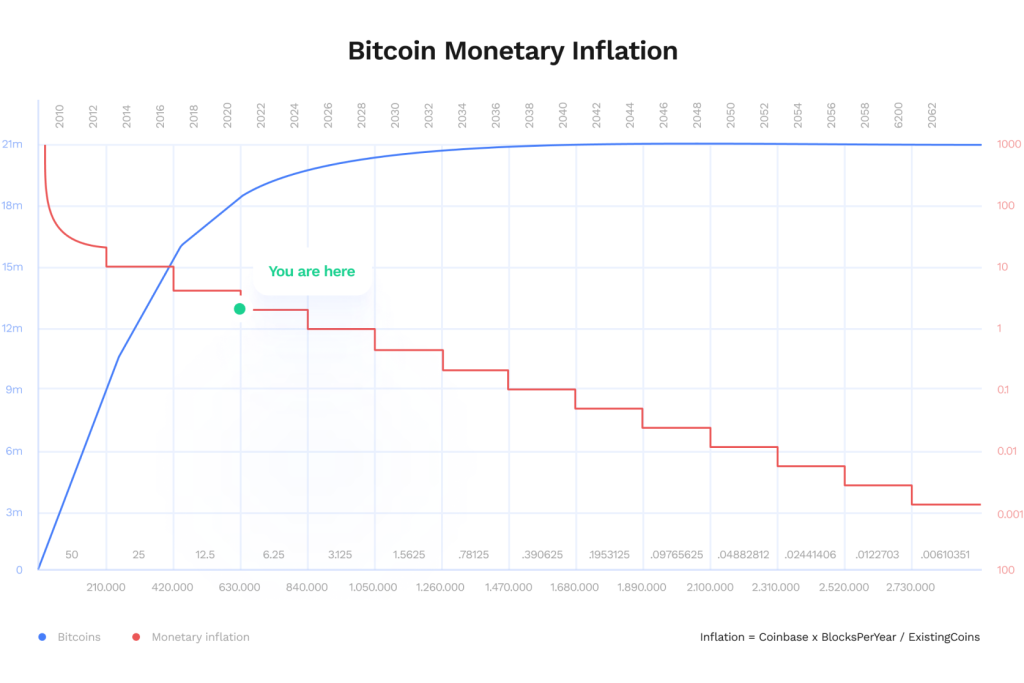

- The mining reward began at 50 BTC in 2009, but halves every 210,000 blocks – roughly four years. There have been three so-called halvings – the last in May 2020 – with the block reward now set at 6.25 BTC.

- This fixed supply schedule will continue until a maximum of 21 million bitcoin are created.

- There is no other way that bitcoin can be created

- Along with the block reward, successful Miners also receive fees that each transaction pays to be sent over the network

The importance of Bitcoin’s fixed supply schedule to perceived value cannot be overstated. It enables us to know Bitcoin’s inflation rate over time – its programmed scarcity.

It also tells us that as of January 2022, 90% of Bitcoin supply has been mined and that the maximum supply will be reached in around 2140, at which point the only reward Miners will receive will be the transaction fees.

The supply schedule is a critical piece of the tokenomics puzzle. If a coin has a maximum supply this tells you that over time inflation will decline to zero, at the point the last coins are mined (see the graph above). This quality is described as disinflationary – as supply increases but at a decreasing marginal rate – and is a valuable characteristic for something to function as a store of value.

If there is no maximum supply this means that tokens will keep being created indefinitely, and potentially diluting value. This is true of the existing fiat monetary system, and one of its biggest criticisms along withe the uncertainty that surrounds the changes in supply.

To know whether the supply of fiat money is expanding or contracting – with the obvious knock on effects to the its purchasing power and the wider economy – you have to wait anxiously for the outcome of periodic closed door Federal Reserve or ECB meetings. Contrast that with the certainty that Bitcoin’s fixed supply schedule provides, which even allows scarcity-based models to predict its value.

Supply Metrics

As the first example of a cryptocurrency, Bitcoin effectively introduced the concept of tokenomics, along with a set of metrics that breakdown the supply schedule of any cryptocurrency into key components that give valuable insight into potential, or comparative, value.

These common yardsticks are published on popular crypto price comparison sites like Coinmarketcap or Coingecko as a complement to the headline price and volume data.

- Maximum Supply – A hard cap on the total number of coins that will ever exist. In the case of Bitcoin 21 million.

- Disinflationary – Coins with a maximum supply are described as disinflationary or deflationary, because the marginal supply increase decreases over time.

- Inflationary – Coins without a maximum supply are described as inflationary because the supply will constantly grow – inflate – over time, which may decrease the purchasing power of existing coins.

- Total Supply – The total number of coins in existence right now.

- Circulating Supply – The best guess of the total number of coins circulating in the public’s hands right now. In the case of Bitcoin, Total Supply and Circulating Supply are the same thing because its distribution was broadcast from day one.

- Market Capitalisation – The Circulating Supply multiplied by current price; this is the main metric for measuring the overall value and importance of a cryptocurrency, just as it is for public companies which multiply share price by number of tradable shares.

- Generally abbreviated to Marketcap, it is often used as a proxy measure for value, and though it is helpful in a comparative sense, its reliance on price means that it reflects what the last person was prepared to pay, which is a very different thing to estimating fundamental value.

- Fully Diluted Market Capitalisation – The maximum supply multiplied by current price; this projects an overall value of the fully supplied coin, but based on current price.

2. Supply Distribution

Whereas the Supply Schedule tells you what the currently Circulating Supply is and the rate at which coins are being created, Supply Distribution takes into consideration how coins are spread among addresses, which can have a big influence on value, and is another important part of tokenomics.

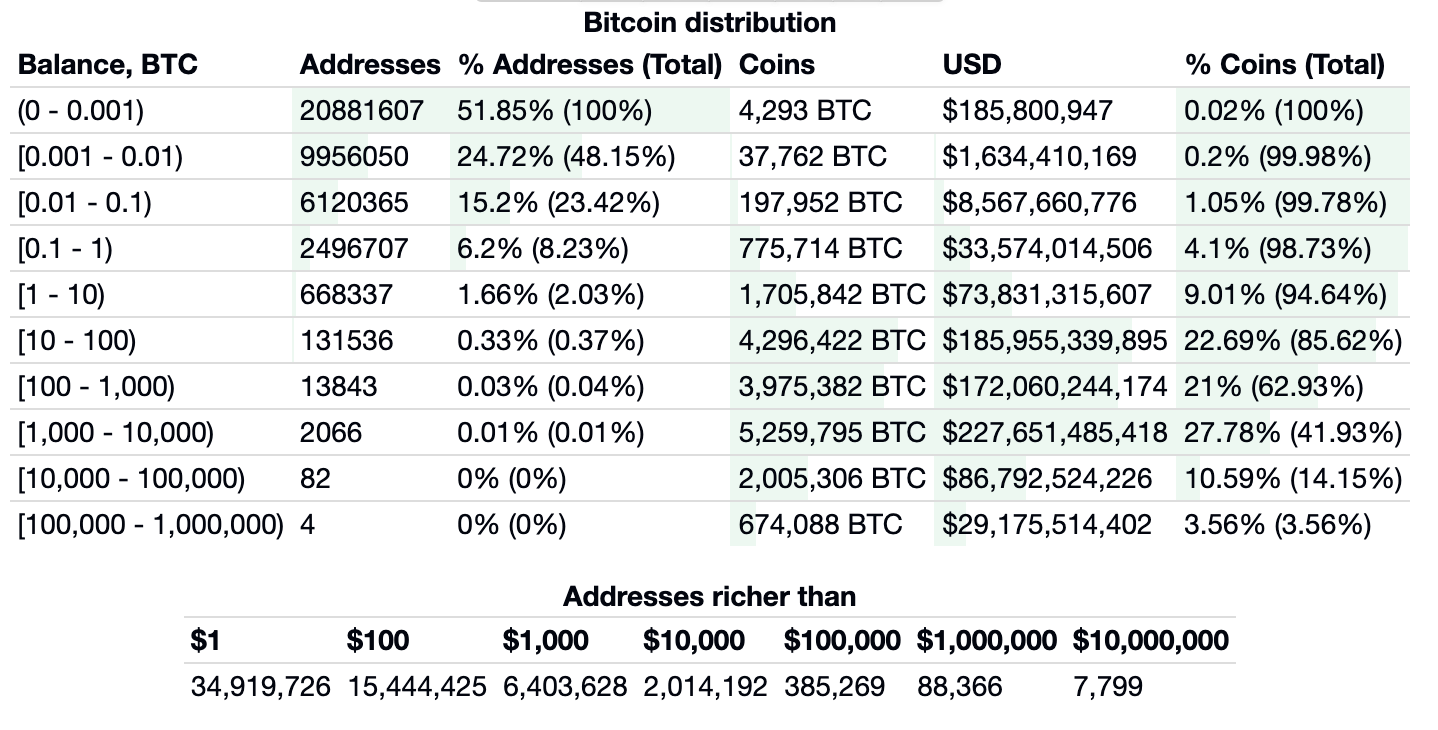

Given cryptocurrencies like Bitcoin are open source, this information is freely available to anyone with an internet connection and some data analysis skills. Here’s the distribution of Bitcoin as of January 2022 courtesy of Bitinfocharts.com.

The raw supply distribution for Bitcoin doesn’t look particularly healthy, with less than 1% of addresses owning 86% of coins, which would suggest that is vulnerable to the actions of the smaller controlling addresses.

But this picture is somewhat misleading, as an individual will have numerous addresses, while one address might belong to an entity – like an exchange – which holds custody of Bitcoin on behalf of potentially millions of users.

Analysis by blockchain analytics provider, Glassnode, suggests that concentration is nowhere near as dramatic, and that the relative amount of bitcoin held by smaller entities has been consistently growing over time.

So though the Bitcoin blockchain is transparent, address ownership is pseudonymous, which means that we can infer certain information about the concentration of crypto ownership, and use this to provide insight in to value, but never really know the true supply distribution at a granular level.

This has spawned an entirely new field of analysis called on-chain analytics – the closest thing to blockchain economics – which uses patterns in address behaviour to infer future price movement.

Lost or Burned Coins

Another factor that further muddies the waters around supply distribution is the number of coins that can never be spent because their Private Keys are lost, or they have been sent to a burn address.

Though there are some well-publicised cases where significant amounts of bitcoin have been lost, it is impossible to put an exact figure on the total amount of lost coins for any cryptocurrency.

Dormancy – a measure of how long addresses have been inactive – is the main hint that on-chain analysts use to calculate how many coins are genuinely lost. Studies estimate that around 3 million bitcoin are irretrievable, which equates to over 14% of the Maximum Supply.

This is an important consideration as price is a function of demand and supply. If the supply of available coins is actually smaller than thought, but demand is unchanged, existing coins become more valuable. This is another reason why Marketcap can be misleading, because it cannot account for lost or burned coins.

Intentionally burning Bitcoin – by sending to an address that is known to be irretrievable – is for obvious reasons, very rare. Burning coins is, however, an important concept in inflationary coins as way to counteract supply growth and the negative impact on price.

Unfortunately, burning generally happens as a manual action, without warning, because it is associated with price increases. Burning can be used programmatically to reduce supply inflation in uncapped cryptocurrencies, as we’ll see with Ethereum below.

As if measuring supply distribution data wasn’t hard enough, there is another crucial consideration impacting value, that raw data doesn’t account for, which is how coins can be shared out before a project is even launched.

If we compare crypto’s two dominant currencies – Bitcoin and Ether – were distributed at launch, we can understand why that is so important.

Bitcoin’s Sacred Launch

Bitcoin was the first cryptocurrency, created in 2008. We don’t know who created it, we just have a pseudonym, Satoshi Nakamoto, who disappeared soon after it was up and running. Their last public communication was in December, 2010.

The creation of Bitcoin is sometimes called a Sacred Launch, because of the manner in which it started is exactly how it runs now. No deals were cut, no venture capitalists involved, no shareholders. No initial distribution to vested parties.

Given what we now know about the relationship of supply distribution to value, Bitcoin’s Sacred Launch is a significant part of its appeal. But though Satoshi didn’t award his/herself a huge stack of coins for creating Bitcoin, they had to play the role of sole Miner until others were convinced to do so, and therefore were earning the 50 BTC reward every 10 minutes for a considerable time.

Much is made of what is described as Satoshi’s coins, the vast amount of bitcoin earned when he/she was the only one mining it in the months after launch.

The addresses that hold it amount to around 1.1 million coins, none of which have ever moved, accounting for one of the four addresses holding 100,000 to 1 million bitcoin in the chart above.

Even rumours that they Satoshi’s coins have moved can have a huge impact on price, showing that tokenomics is not just a matter of numbers, but includes elements of behavioural analysis, inference and game theory.

Though a significant amount of bitcoin is definitely in a few hands, it’s Sacred Launch and permissionless nature are regarded as features, rather than bugs.

Most of the cryptocurrencies that followed however, took a different approach to their launch and how supply was initially distributed.

Ethereum & the concept of Premine

It turns out that the initial approach taken by Satoshi was the exception, rather than the rule, largely because the majority of cryptocurrencies that followed were created by a known team, and supported by early investors, both of whom were rewarded with coins before the network was up and running.

One of the reasons why skeptics think crypto has no value is because of the idea that, given its virtual nature, it can just be created out of thin air. In many cases that is actually what happens with the initial distribution of a new coin, aka a Premine.

The idea of a Premine began with the launch of Ethereum in 2013. Rather than a Sacred Launch, Ethereum’s founders decided on an initial distribution of Ether – the native token – that included those who were part of the original team, developers and community with a portion set aside for early investors, through what was known as the Initial Coin Offering (ICO).

The Premine was essentially crypto’s way of using a traditional form of equity distribution to reward entrepreneurs with a stake in their creation, but can put a significant proportion of the overall supply in very few hands, and depending on what restrictions are placed on selling, can tell you a lot about how focused the founders are on creating long term value, or short term personal gain.

The ICO used a completely new approach to investing in a tech start-up, attempting to give everyone an equal chance to invest, by setting aside a fixed amount on a first-come-first-served basis, which – in the case of Ethereum’s launch – simply required an investor to sending bitcoin to a specific address.

This was intended to counter the privileged access that venture capital has to privately investing in emerging companies. That was the theory, things didn’t quite work out in practice.

Unfortunately Premines and ICOs quickly got out of control, and the idea of democratising early stage investment soon evaporated. Initial allocations incentivised hype and over-promise, while ICOs were set by FOMO and greed.

- If you had enough ETH you could game the system by paying ridiculous fees & frontrunning

- In many cases ICOs were staggered, with privileged access to early investors or brokers

Premines and visible founders are two of the biggest arguments used by Bitcoin Maximalists who feel that only Bitcoin provides genuine decentralisation because it has no single controlling figure, and has a vast network of Nodes that all have to agree on potential rule changes.

This is why tokenomics must include some measure of decentralisation, because even if a cryptocurrency has a maximum supply, its founders are capable of simply rewriting the rules in their favour, or simply disappearing in a so-called rug pull.

Address distribution should be a consideration when trying to understand what value a cryptocurrency has. The more diverse ownership is, the lower the chance that price can be impacted by own holder or a small group of holders.

Node Distribution

Just as concentration of supply within a few hands is unhealthy, if there are only a small number of miners/validators, the threshold to force a change to the supply schedule is relatively low, which could also devastate value.

In the same way, the distribution of those that run the network – the Nodes and Validators – has a crucial influence. Nodes enforce the rules that govern how a cryptocurrency works, including the supply schedule and consensus method already mentioned.

If there is only a small number of Nodes, they can collude to enforce a different version of those rules or to gain a majority agreement on a different version of the blockchain record the network holds (aka a 51% attack).

Either scenario means there is no certainty that the tokenomics can be relied up, which negatively impacts potential value.

3. Tokenomics & Incentives

Another important consideration of tokenomics are the incentives users have to play some role in a cryptocurrency’s function. The most explicit reward is that provided for processing new blocks of transactions, which differs depending on the consensus method used; the two main methods having already been introduced.

Mining (PoW) – Being rewarded for processing transactions by running mining algorithms for Proof of Work blockchains, like Bitcoin

Validating/Staking (PoS) – Being rewarded for validating transactions by staking funds in Proof of Stake blockchains.

Blockchains are self-organising. They don’t recruit or contract Miners or Validators, they simply join the network because of the economic incentive for providing a service. The byproduct of more Nodes is an increase in the resilience and independence of the network.

Being directly involved as a Miner or Validator requires technical knowledge, and up-front costs, such as specialist equipment, which in the case of Bitcoin means industrial scale operations beyond the budget of solo miners, and in the case of Ethereum, a minimum stake of 32 ETH.

But as the crypto ecosystem has become more sophisticated opportunities to passively generate income, by indirectly staking and mining, have grown dramatically.

Users can simply stake funds for PoS chains with a few clicks within a supported wallet and generate a passive income, or add their Bitcoin to a Mining Pool to generate a share of the aggregate mining rewards.

Ethereum will experience a significant change in its tokenomics in 2022, changing from a Proof of Work consensus mechanism to Proof of Stake. ETH holders have been able to stake since December 2020, when Ethereum 2.0 launched.

Total Value Locked (TVL) provides a measure of how much Ethereum has been staked, while figures are also available for how much ETH is now being burned, and the impact on overall supply.

Both these metrics are being interpreted positively by supporters of Ethereum, but its detractors simply say that the ability to make wholesale changes to its governing principles illustrates weakness, not strength.

How successful chains are at attracting this financial backing has a significant impact on price, especially where funds are locked for a given period as part of the commitment, as this provides price stability.

The impact of fees

Whatever consensus method a cryptocurrency uses, it can only grow if there is demand for transactions from users, which will be influenced by:

- the cost of making a transaction, how it is calculated & who earns it

- how fast a transaction is processed

Fees and Miner/Validator revenue are two sides of the same coin, providing a barometer of blockchain usage and health. Low fees can incentivise usage; while an active and growing user base attracts more Miners/Validators, keen to earn fees. This creates network effects, generating value for all participants in a win-win situation.

Fees are especially important where they pay for computational power, rather than just the processing of transactions. This type of blockchain emerged in the years following Bitcoin’s launch, starting with Ethereum, known as the world’s computer. It provides processes the majority of transactions related to the growth areas of DEFI and NFTs, but has become a victim of its own success with its fees – measured in something called GAS – pricing out all but the wealthiest users.

Addressing that challenge is one of the key objectives of the changes in the Ethereum Roadmap. EIP 1559 – aka the London Upgrade – which happened in August 2021.

Not only did the fee estimation process completely change, with the aim of making fees cheaper, the changes to Ethereum’s fee structure are also having a significant impact on its tokenomics. Instead of all transaction fees going to Ethereum Miners, a mechanism was introduced to burn a portion of fees turning it from inflationary (no maximum supply cap) to disinflationary.

Consensus methods and fee structures can therefore, provide important incentives for participation in a blockchain ecosystem, and even directly impact supply, so should be considered as part of tokenomics. There are also a number of other incentives and influences that complete the tokenomics picture.

IEOs, IDOs & Bonding Curves

ICOs failed because they fuelled bad behaviour from both entrepreneurs, with exit scams and untested ideas, and from investors, encouraging short term speculation, rather than actual usage.

What has emerged are more innovative ways to incentivise ownership and usage of tokens – as intended – that learn from these mistakes.

One approach to launching is to negotiate directly with centralised exchanges to ensure they are listed and tap into the existing base of users – known as an IEO – Initial Exchange Offering. This can have a significant impact on ownership distribution and price, as illustrated by the well publicised price boost that coins listed on Coinbase experience. But this is a long way from Bitcoin’s organic, decentralised debut.

IEOs put all the power in the hands of the large exchanges, who will pick and choose coins that they deem anticipate demand for. But given crypto is about removing the middleman, one of the most interesting developments in coin launches is the IDO – Initial Decentralised Exchange Offering.

An IDO is a programmatic way of listing a new token on a Decentralised Exchange (DEX) using Ethereum Smart Contracts and mathematics to shape incentives for buying and selling through something called a Bonding Curve.

Bonding Curves create a fixed price discovery mechanism based on supply and demand of a new token, relative to the price of Ethereum. Their complexity warrants a completely separate article, but it is enough to know that the shape of bonding curves is relevant to the tokenomics of new ERC20 coins launched on DEXs or DEFI platforms, because it can incentivise the timing of investment.

While bonding curves a mathematically complex way to incentivise investment in the new cryptocurrencies, there are more obvious and cruder approaches, particularly within DEFI, where the focus is providing interest on tokens. as a way to encourage early investment.

APYs & Ponzinomics

DEFI has exploded over the last 18 months, with over $90bn in TVL according to Defi Pulse, but this has also fuelled a mania around APY (average percentage yield).

Many tokens have no real use case other than incentivising users to buy and stake/lock-up the coin in order to generate early liquidity. This doesn’t reward positive behaviour, but simply creates a race to the bottom, with users chasing ludicrous returns then dumping coins before the interest rates inevitably crash. This approach has been nicknamed Ponzinomics as the ongoing function of the token is unsustainable.

Airdrops

There is another way to reward holders in terms of how much they have actually used the token as it was intended – Airdrops. DEFI projects like Uniswap and 1Inch are good examples, while OpenSea did the same for those most active in minting and trading NFTs.

Airdrops are financed from the initial treasury but unfortunately aren’t built into road maps, as telegraphing them would be self-defeating.

Many savvy investors simply use new DEFI, NFT or Metaverse platforms simply in the hope, or expectation, of an Airdrop. That makes them relevant to tokenomics as they will drastically alter supply distribution of a token, but given the secrecy that surrounds them, can only be factored into retrospectively.

DAOs & Governance

We’ve already discussed how the concentration of ownership and the network impacts perceived value, given the concern that control rests in a few hands. Even where there is a healthy distribution of holding addresses, they are largely passive, and have no specific influence on how the cryptocurrency functions.

There is a growing move towards crypto projects that are actively run by their communities through DAOs (Decentralised Autonomous Organisations).

DAOs give holders of the native token the right to actively participate in its governance. Token holders can submit proposals and receive votes, in proportion to their holdings, on which proposals are accepted . DAOs therefore have a crucial influence on tokenomics because the community can decide to tweak or even rip up the rules.

DAOs are essentially attempts to create a new digital democracy via crypto, and still have a lot of hurdles to overcome, as rational rules have to be written by irrational humans.

Tokenomics & Rational Decision Making

Sensible tokenomics doesn’t guarantee a project will succeed, nor does a blatantly vague token model doom a coin to failure.

For every project that makes huge efforts toward transparent supply schedules, good governance and healthy incentives for using of the network, there are hundreds, if not thousands, that have fuzzy or non-existent distribution logic because sensible tokenomics isn’t their aim, they simply want to meme, or hustle their way to higher market capitalisation.

Coins like Dogecoin or Shiba Inu have crazy supply schedules yet can still generate a huge market cap – bigger than global publicly traded brands – because investors are irrational.

So studying tokenomics on its own doesn’t mean that you can find cryptocurrencies that will succeed and increase in price, as you have to also understand how other people are making decisions, many of whom have no interest in tokenomics, or even know what it means.

What tokenomics does give you is a framework to understand how a coin is intended to work, which can form part of an investing decision.

Here’s a summary of what the main metrics can tell you:

- Maximum supply – Positive indicator for an effective store of value; if there is no supply cap, there will be ongoing inflation, which may dilute the value of all existing coins.Network/Nodes – The more diverse the better. Will make arbitrary decisions less likely, producing stability.

- Supply Distribution – The more evenly distributed the better, as there is less chance that one person can have a disproportionate impact on price by selling their coins

- Fee Revenue – Shows you how much people are actively using it; a proxy for cashflow

- TVL Locked – Shows that users are willing to put their money where their mouth is, and lock in their investment for a share of rewards

- Governance, Airdrops, Incentives & launch strategies can all influence supply distribution so should be considered as part of tokenomics.

So much about the crypto ecosystem is novel and disrupt…